After years of consistently writing posts on this blog you may have noticed that the blog suffered a rather sudden and silent death. Whilst I never intended to just disappear there was a very deliberate reason I stepped away from blogging...

While I love blogging about financial topics and personal finance, I found that I was spending far more time talking about finance and investments rather than taking control of my own financial life.

It doesn't mean that I was not doing the things I was saying that I was doing. There was just a lot of "this month I will do x, y and z" and honestly a lot of that stuff never got done.

In addition to this I decided that I needed to concentrate far more on my career and my time at home got taken up with a new addition to our family.

However I still kept tracking my net worth...

Just because I wasn't writing posts on it every month doesn't mean I let my focus on my net worth and financials fall by the wayside...

Actually with all the time I freed up by not having a posting schedule (and by giving up my industry blog that I started as well) I found that I had far more time to dedicate to my own personal finances. I still track my net worth every month and I my plans have evolved significantly since the last time I posted on here.

I'm going to go through a quick summary of my net worth, the changes that have happened over the last year as well and then will cover quickly what my new plans look like.

June 2017 Net Worth: $1,130,000

I finally cracked the $1 million mark a few months ago however this had as much to do with how I measured my net worth as improvements in my savings and investing focus and outcomes. Before I get into the nitty gritty details here are the highlights:

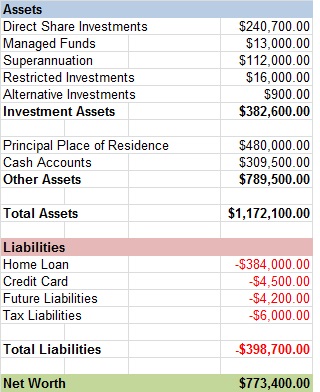

As you can see I have managed to increase my assets significantly over the last year while holding my liabilities flat.

My liabilities are fairly basic - I have a home loan, some credit card debt (which is rolling and I pay it off every month) and some tax liabilities which come due once a year.

My assets are far more complex and over the last year I've spent some time re-working how I think about my assets. Historically I just broke them into categories like shares, property, cash etc. I now take a more nuanced view of my assets which you can see below:

The differences in totals are due to rounding at various asset classes but don't worry my numbers add up on my spreadsheet.

Now that we can see what is actually going on in my asset portfolio we can have a discussion about what I've actually been doing and changing.

Investment assets

Broadly speaking my investment assets fall into two categories that you can see above. Controlled investment assets and restricted investment assets.

Restricted investment assets include my retirement accounts (the majority) and employer restricted shares. I have little to no control over these and I don't add excess amounts to these accounts so let's set them to one side for the moment.

Controlled investment assets are where I've been concentrating my efforts and in the last year these accounts increased by ~60,000.

- My investment holdings have done really well in the last year especially post the election of Donald Trump in November last year (who would have thought?!). I have been selling out shares which have performed particularly well as well as holdings which I am no longer particularly close to

- Years ago my parents gave me some managed funds and I've held onto them for years. However they were incredibly high fee and didn't really outperform the market after tax so I recently sold them and am slowly reinvesting them back into index ETFs and select individual stocks

- Uninvested cash is cash that is sitting there for investment purposes but which I haven't found a home for yet. I don't like this cash balance to get too high and it is sitting a little higher than I would have liked. Most of this is in USD and I'm waiting for the exchange rate to come back before bringing it back

The largest increases in my asset base have been in my non investment assets whose total value increased ~$240,000 over the year

- The Principal Place of Residence as the name suggests is my home. Historically I valued this at the amount I paid for it and a few years ago I increased it from $440,000 to $480,000 when the bank did a revaluation. More recently I've been using a selection of apps which track the market value of my home. Tracking this at historic value may have been conservative but it actually belied the level of equity I had to draw on and the exposure I had to the property market so I've been using market values. My home property market has been on a tear for the last few years which is the cause of the large increase in my home value

- My non investment cash holdings is the cash we are saving to buy our new home with. It offsets most of my liabilities (my home loan) and will be used to pay for our new home. As we are looking to buy a new home in the next year or two this is where we have been concentrating most of our savings efforts

Financial Freedom Targets

When I first started this blog in 2011 I was in my mid 20s and I wanted to be rich. Not just comfortable but rich. In fact as you can tell from the title of this blog I wanted $90m and I was willing to do anything to get there.

Over time my priorities have changed. I value lifestyle and living a full life as far more important than I used to and as such my financial priorities have changed as well. I discovered the FIRE (financial independence retire early) community and a lot of what they had to say inspired and motivated me.

Now I'm not looking to retire particularly early but financial independence and having investment income to cover my living expenses sounds pretty appealing to me. It gives me the flexibility to perhaps pursue a life where I earn slightly less but perhaps get to live a little more.

So I started with a target:

My target is to earn $100,000 p.a. (in 2016 dollars) from investment income

This would cover the lifestyle that I currently live with a bit of a buffer and would allow me to be comfortable even without a job.

I then back solved what this would require in terms of assets:

Obviously this is incredibly dependent on your assumptions and I'm not going to set out all of my assumptions and asset allocation mix here. But basically:

My income target of $100,000 requires $2.8m of total assets (including a home value) in 2016 dollars

Now why do I keep mentioning 2016 dollars? Because inflation eats away at the spending power of your money. $100,000 today is not the same as $100,000 15 years from now.

Accounting for inflation my 2017 asset target is $2.9m and importantly these numbers are net. Meaning I have all my debt paid off. So I'm aiming for $2.9m this year and my net worth is $1.1m which means:

I am currently $1.8m short of achieving financial freedom

This seems like a huge amount to be short by but once you consider that I can save and invest at above inflation rates then I should be able to achieve this target over time

So am I back for good now?

Well...no. I found that being able to concentrate on my investments and career has really started to pay dividends for me and given it's working for me I'm going to continue with it.

That being said my aim is to update my progress on these big goals on occasions. Given that it is a slow moving target I'm currently thinking semi annually seems about right.